I manually audited the top 10,000 Ethereum addresses to learn about liquidity, profitability, market manipulation and what Whales are doing with their money.

This is the first of many reports to come from this data set.

The top 10k addresses represent 91.7M ETH.

The top 1k addresses represent 70.7M ETH.

The top 100 addresses represent 37.8M ETH.

The top 10 addresses represent 16.6M ETH.

Roughly 17% ETH is held by 10 addresses.

Some maximalists my scream that this is too high and proves a “premine” and centralized control.

But, that couldn’t be further from the truth.

The reason ETH’s distribution seems so focused is actually smart contracts.

Unlike some other currencies, ETH actually gets used for a purpose.

A lot of time that purpose requires depositing something into a contract, often in a trustless manner in which you still control the asset.

A great example is wETH where we deposit Ether in order to get Wrapped Ether for standard ERC20 use.

This smart contract usage is what skews the distribution on ETH, and can make it seem like it isn’t fair.

So what happens if we remove the smart contracts and only look at exchanges, individuals and funds?

When we remove the smart contracts the distribution is now:

The top 100 represent 26.4M ETH.

The top 1k represents 42.5M ETH.

The top 10k represents 57.2M ETH. (56.7%)

Maximalists love to say ETH is more centralized than BTC and that the ICO is a “70% premine”

But, what does Bitcoin’s distribution look like when we compare it to ETH directly?

Bitcoin’s Top 10k Holders: 10.54M BTC (57.44%)

Ethereum’s Top 10k Holders: 57.2M ETH (56.70%)

Based on individual holders, Ethereum is as equally distributed as Bitcoin.

How does that stack up to other networks?

In XRP 16 addresses hold 55.2% of XRP.

In BCH 1100 addresses hold 56.8% of BCH

In BSV 1250 addresses hold 55.6% of BSV

In Litecoin 300 addresses hold 54.3% of LTC

In Tron 1031 addresses hold 51.1% of TRX.

This means when it comes to equity of distribution, Ethereum and Bitcoin are in a league of their own.

No other coin comes within an order of magnitude of their distribution.

You would think, like most people, that there is 110,696,890 ETH.

This is already where you’d start to be wrong.

Most automated on-chain calculations account only for how much ETH was ever created.

They fail to account for how much ETH is lost or inaccessible. That’s something you can only do manually.

We identified at least 6.2M ETH that is confirmed burned/lost, and another 3.8M ETH that is likely lost or burned.

That means that roughly 9% of ETH is inaccessible and there is actually only around 100M ETH in circulation.

That may not sound like a big difference, but it *REALLY* matters when we talk about ETH2.0 sharding returns.

The fantastic team at ETHHub, has a nice chart for us to review the staking rewards based on amount of ETH validating.

It gets down to GIC rates at 100M staked. Which we know won’t be the case, as that would leave ETH with a very low liquidity.

We know about 65M ETH is “active”. We can remove the 26M ETH from exchange hot wallets, and assume that an additional 20% of ETH stays active in contracts and payments.

That brings us down to 76.2M ETH.

We can also remove the 6.1M burned ETH, 3.8M likely lost ETH, and 1.7M locked ETH.

But, what about cold exchange wallets?

Exchanges maintain strong cold wallet reserves, and most exchanges do not take a fraction reserve approach. But, this could change under ETH2.0 due to the staking rewards.

Let’s assume that some major exchanges will keep full reserves, and some sketchy ones will keep next to no reserves. We’ll assume that 80% of cold exchange funds stay cold.

That means we can remove another 20M ETH.

Which leaves us with 44.6M ETH that is currently in a position where it could likely enter into staking.

But that is the absolute max amount.

So how would we estimate how much ETH likely WILL be staked?

We’d base that on a distribution — and usually in tech we use a distribution model that is a slightly adapted standard distribution.

It comes from a theory called crossing the chasm.

Basically this means we expect adoption of a new tech to come in waves.

2.5% innovators.

13.5% early adopters.

34% early majority.

These waves are ultimately based on product maturity.

It is a bit hard to calculate how much of that 44.6M ETH would fall into each tranche.

Because the percentage in crossing the chasm is not based on the ETH balance.

It’s based on the number of holders — which is not a standard distribution.

But, as a rough estimate.

2.5% would be 1.15M ETH

13.5% would be 6M ETH (7.15M ETH total)

34% would be 15.1M ETH (22.3M ETH total)

So we could estimate:

Early Phase 0 staking would be 17%-20% yield.

Dropping to 6% — 8% once staking services are more robust and common place.

Leveling off at 4%-6% once ETH2.0 is rolled out and transactable.

Those early returns don’t account for EIP-1559 burning, or increase in ETH price.

And as we know, ETH2.0’s roll out will cause some serious price action:

So I guess we can call that conclusions:

That’s it.

That’s the tweet.

64.53% of top ETH was ‘active’ meaning it had been on an exchange or spent in the past 30 days.

14.02% was in cold wallets (1+ year idle)

9.71% was idle (31–364 days no activity)

1.76% was locked in time locked contracts

That may not seem that shocking at first, but, compare it to the stats across all Ethereum addresses.

Where 54.39% of addresses are cold (1 year+) and 39.93% of addresses are idle. With only 5.68% being active.

So what does this mean?

It means our 4th finding

It means that whale accounts are very active in this down market, and many of them have been accumulating.

Existing whales have increased their position by more than 4% in the past 6 months. ($550M USD)

That rivals the roughly $600M in new capital influx that Bitcoin was estimated to see last year.

But, for Ethereum, that was only on whale accounts, and only in the past 6 months.

Whales love ETH & BTC. Nothing else has this level of inflow.

But perhaps more important is

There are a SIGNIFICANT number of new wallets in the top 10k who had their first transaction associated with fiat onramp exchanges that serve large scale customers (mostly Gemini, Kraken and Coinbase)

These new addresses often bought $100,000 — $250,000 worth of Ethereum, and they represent around 6% of the top 10,000 addresses. (Or ~$100M in new ETH purchases in the past 6 months)

Let’s repeat that in its own tweet, so you can retweet it at naysayers.

In the past 6 months, whales have bought more than $650M in new Ethereum purchases.

That means in the past 6 months, whales have bought more Ethereum, than all new Bitcoin inflow last year.

There now back to more data.

Right now, 33.6M ETH is deposited into exchanges.

With only 13.7M of that is in cold wallets, with the rest being in hot wallets.

This means the average exchange has only around 40% of their holdings in cold reserves.

But, among that there are some winners and losers:

BitFlyer, Gate.io, Coinbase and Kraken have the best ratios of cold to hot holdings.

Up to 78% cold.

They don’t take chances with your crypto.

On the other hand Yobit, Poloniex and Bithumb rely way too heavily on hot wallets.

Up to 91%.

Yikes.

Speaking of Poloniex…

When Circle bought Poloniex, they responsibly moved assets to better cold wallets and had strong reserves.

Around the time that Tron took over Poloniex, it seems some cold wallets drained. Not entirely, just to fractional reserves.

Which is odd.

If Circle was taking the assets, they would have fully drained the wallets. So why did Poloniex seem to go lower liquidity?

Those wallets then drained into exchanges, but, only exchanges that listed Tron.

Around this time, BEFORE the announcement, there was an increase in buying activity on Tron.

TRX’s price rose around 50% (from $0.14 to $0.21).

Did Tron switch Poloniex to fractional reserves to pump their own token price?

It might justify the high price paid for a dying exchange?

The price action might be unrelated, and Poloniex may simply be cross-market trading on other exchanges.

But the sudden shift in cold wallet balance is concerning.

Back to the ETH data!

Right now, there is only 19.5M ETH listed on exchanges for sale.

Even though 33.6M ETH is deposited in exchanges.

That’s only 58% of deposits, so whales are accumulating, not selling.

For comparison, that number has been historically more than 75%+ any time the Eth price has risen by >25%.

This is the first time ever, that ETH has risen >50% and the number has been below 80%.

Whales are hungry.

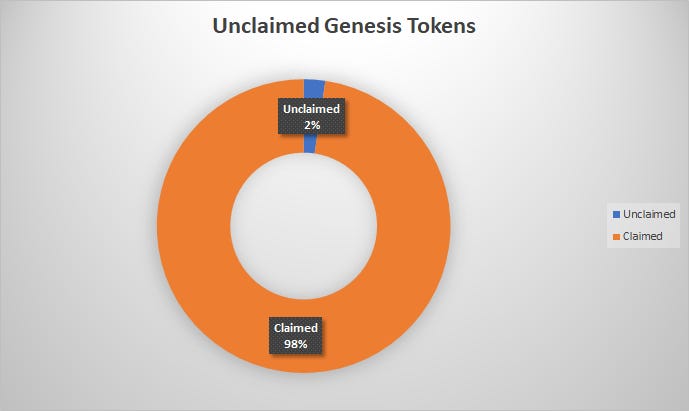

347 Genesis addresses in the top 10k failed to ever claim their ETH ICO purchase.

These idle funds are 1.7M ETH or around $340M USD.

There are likely additional long tail Genesis wallet addresses that are unclaimed as well.

But, these funds, if staked could generate more than $5M annually.

It may be worth the Ethereum community debating forking unclaimed funds in ETH2.0, staking them, and using the revenue for community based funding.

Speaking of Genesis wallets, most founding ETH members who were in the top list still hold most of their funds.

On average dev grant and founders still hold 56.4% of their original genesis Ether.

Only two early grant holders who were in the top list heavily sold ETH. In both cases this was to fund large businesses in the crypto space that have struggled with revenue.

At least two founding members have also not ever touched their genesis grants.

What about Vitalik?

At peak Vitalik likely had ~630,000 ETH.

At least 54,856 was allocated in donations to external entities personally.

167,000 was sold before 2018.

He put an additional 50,000 into EthDev

35,000 for funding additional ecosystem projects

That means Vitalik only sold around 26% of his ETH holdings over the past 5 years, most of it when ETH was low in price.

On the other hand, he has donated at least 21% of his ETH to supporting the ecosystem, and he holds the remainder.

This dismantles the narrative of Ethereum being a founder based scam.

Vitalik owned, at max 0.9% of ETH.

For every ETH he has sold, he has donated the equivalent to the ecosystem.

This goes to show that Vitalik believes in the vision of Ethereum isn’t here for a get rich quick scheme and puts his money where his mouth is.

But, perhaps most importantly, that nearly all EF founders are in the same boat.

Of the Genesis Buyers in the top list that claimed their wallets, 97.4% of them still hold >75% of their initial ETH purchased.

They are also token purists, with 97.4% of them never having purchased any tokens.

Among Genesis & Top 250 individual accounts, the only tokens we see are ANT, BAT, ENG, ENJ, GNO, GNT, HOT, KNC, LINK, MKR, MLN, OMG, POWR, QSP, RDN, REN, REP, TKN, ZRX & TokenSets.

In all cases the tokens are only owned by 1–2 addresses each.

Out of the top 10k wallets, the average balance is 9,170 ETH ($1.8M).

That’s fairly bias by exchanges. The median amount is 1,672 ETH ($334,000)

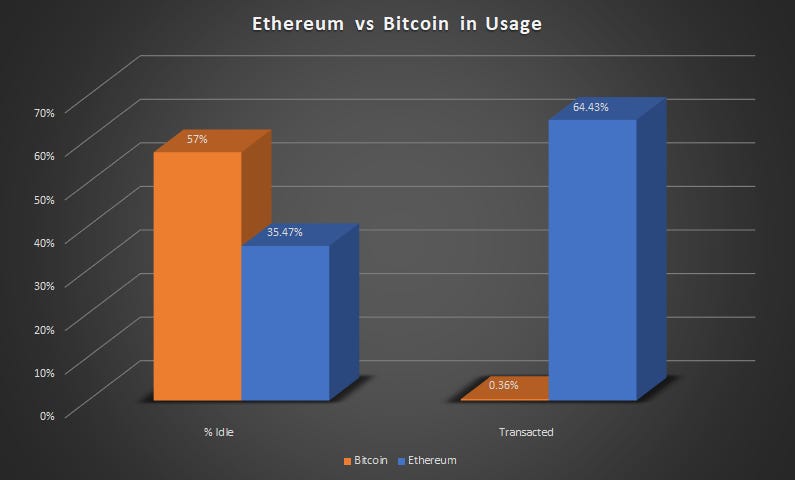

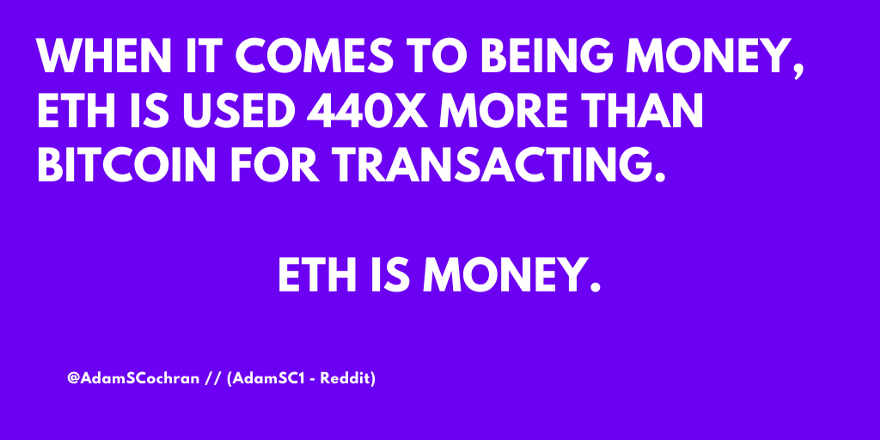

16.2M ETH is in ‘active’ circulation meaning in the last 90 days it passed through a payment processor, payment gateway or smart contract (excluding exchange and multisig.)

That means ETH is actually being *HEAVILY* used as money and gas.

Compare that to Bitcoin where 57% of Bitcoin hasn’t moved in over a year (with 21% not moving since 2015).

And only 0.36% of Bitcoin has been through a payment processor in the past two-years.

When it comes to being money, ETH is used 440x more than Bitcoin for transacting.

ETH is money.

Plain, simple, and re-tweetable.

In a strange twist, miners are starting to horde. In the past 6 months miners have accumulated 1.15M ETH ($230M USD) that they haven’t sold.

This is strange because miners have hard costs to cover in their mining operations so they very rarely ever horde any ETH at all.

We’ve never seen such a rapid increase in miner hording on ETH. Ever.

It seems likely that as we edge closer to Phase0 roll out, ETH miners are getting ready to convert mining operations into staking operations.

Which will lower their costs. However, some miners continue to heavily sell, possibly indicating they won’t be stakers in the future.

This hording seems to be only around 20% of miners, but, they are hording at aggressive levels.

This may mean we see around 80% of miners shift to other PoW chains. Which could be great for ETH’s little brother ETC.

It also means we have a chance to further improve decentralization if we can make it easy for users to host their own nodes on low end hardware.

Either way, profiteering miners are bullish on the future of ETH.

In the past 6 months, exchange deposits grew ~5x from 11,000 a day to >55,000 a day.

This is normally the leading early indicator of a bear market or mass sell-off.

Instead, those sell walls got chewed up by whales. Despite the 5x increase in volume, ETH rose in price.

This tells you the remarkable confidence that large investors have in ETH right now.

The last 3 times we saw exchange deposits grow by 4–5x in under a one-month span, lead to market drops >40% of the price.

This is the only time I’ve been able to identify the inverse. There is a major positive sentiment being shown in the market right now.

There are a group of at least 12 whales, that in coordination with BitFinex (and maybe BitMex?) seem to manipulate the market.

Their attack works as follows:

First, we see an increase in people shorting ETH. It usually starts on BitFinex, and then expands to BitMex and finally other exchanges.

These whales start sending equal batch transactions over a few days to BitFinex, Coinbase, Kraken, Bitstamp, Bitflyer

They make repeated small transactions so that systems like WhaleAlerts don’t pick up on the transaction.

Then all at once, the market dumps. They profit on their huge shorts and buy back at a lower price.

Once its done, they batch transactions back to their addresses.

It sometimes takes them more than two weeks to migrate their ETH back, but, its always with a profit. Usually these wallets continue to buy new ETH for 4–6 weeks after their dump.

What gets really interesting is that BitFinex cold wallets often seem to get in on this dumping action about 40% of the time, which is surprising given how rarely cold wallets move.

Speaking of Bitfinex,

BitFinex withdraw 1.17M ETH from their hot wallets to cold wallets to take place in the CarbonVote on ProgPow.

https://web.archive.org/web/20190402164923/http://www.progpowcarbonvote.com/

Only around 3M Ethereum was involved in the voting process, meaning that BitFinex represented >40% of the vote.

And, this isn’t the only vote manipulation that happened around ProgPow.

With swirling acusations around NVIDIA and AMD, and a GPU data center helping to fund ProgPoW (https://www.trustnodes.com/2019/01/10/rumors-circulate-after-eth-devs-suddenly-decide-a-proof-of-work-change) it’s no surprise that we identified 36 other cold addresses that sprug to life to vote in favor of ProgPow and went idle again.

This validates what most people suspected.

The community doesn’t want ProgPoW.

Big self-interested parties want ProgPow.

On the topic of exchanges:

The exchange that best obscures transactions is actually Coinbase.

They spin up new wallets and mix funds on all outbound transactions making it really hard to identify.

We were able to identify the source and destination of 80% of transactions from all other exchanges with ease.

Only Coinbase (and Tornado.cash) made it more difficult.

We were also able to identify wallets associated with major players such as JPMorgan Chase, Reddit, IBM, Microsoft, Amazon and Walmart.

100% of these wallets are accumulating ETH.

It is unclear to what end, and where it sits in their corporate structure/if it is an official corporate initiative or not.

What is clear, is they are growing at this price point and betting on ETH in someway.

The individuals on the top whale list who grew their net worth the most over the past 3 years were those who were patient.

They always sold very little of their stack.

They also never bought tokens at ICO, they always waited till a few months after coins were listed places and dropped down in price.

There is a lot of anti-ETH rhetoric out there.

A lot of it coming from BTC maxis. But, where does that disinformation start?

Some whale addresses helped me clue in.

First, I mapped address moves vs tweet volume and tweet sentiment related to ETH.

The first thing I noticed is that negative ETH sentiments do occasionally shift the price downward.

This is “shaking out weak hands” — mostly ETH novices who don’t know enough to shrug off the disinformation.

Then I noticed that buying action from whales surges after this sell off.

That makes sense. Whales move money in to exchanges to buy more ETH when the market drops.

But, this is where it gets really interesting.

There are multiple addresses that shift USDC, USDT, DAI and Paxos into exchanges BEFORE large spikes in anti-ETH tweets (both spikes in volume and negative sentiment)

Most Whale addresses move money in AFTER the social spike, and only respond to about 8% of spikes.

However, a handful of addresses (seemingly out of Asia and Europe) move the assets, almost without fail, BEFORE the shift in sentiment.

How often do these magical addresses seem to predict new increases in negative tweets?

Roughly 86.7% of the time…..

You don’t need to be a data scientist to realize that level of correlation is highly suspect.

Now, not all of these negative sentiment spikes are effective in moving the price.

In fact, it works less than 7% of the time. But, when it works, it works well.

And these whales are somehow always magically ready to capture it.

Which likely suggests that these addresses are actually funding ETH FUD or spreading it via bots so they can accumulate.

That sounds like a bad thing — but, if the funding for most of the hate about your project, comes from people who are simply trying to get in on the project at a better price — that says something about your quality and your future.

For what its worth, I (so far) do not believe that any of the BTC maxi’s who are anti-ETH are complicit in this manipulation.

It’s more likely they are getting anonymous tips/funding funneled to them, and bots retweeting their sentiment.

But it is something I plan to investigate further, as there would be some sweet sweet irony-filled justice if some of the top BTC maxis were funded by ETH money :)

You are on average, only roughly 12 wallet transactions away from a genesis block.

It’s the Ethereum equivelent of your ‘(Kevin) Bacon Number’ — Buterin Number is perhaps the best term here?

There are only 8 addresses in the top 10,000 that are not from genesis and have no transfers.

They are 8 solo miners who accumulated their wealth through early mining.

All are active wallets and seem to have no interest in selling.

In the top 250 wallets only TokenSets, Tornado.Cash and Maker have been used by individually owned wallets.

In the top 10k we also find Uniswap, Aave, Bancor, Compound, Kyber, Loopring, Nexus Mutual, Melon and Augur.

So far, these are used by less than 6% of the top 10k wallets, which means that DeFi still has incredible room for growth.

With $800M locked in DeFi — most of it comes from individual micro wallets.

Wait till whales catch on!

While not many whales are involved yet, the amount of ETH whales have put into DeFi has more than doubled over the past 6 months, with them expanding their positions in all of the above projects except for Loopring, Melon and Augur.

In the end this is all extremely bullish for Ethereum.

Let’s recap:

Whales are increasing their stake.

New whales are funneling in.

Eth is more transacted than BTC.

There was more capital inflow into ETH than to BTC.

There is less ETH than you thought.

Not that much ETH can stake first round.

Staking returns could be as high as 17% early on.

Whales are accumulating.

Haters are accumulating.

Miners are accumulating.

Eth is as decentralized as Bitcoin.

ETH founders still hold most of their ETH.

Vitalik donates 1 ETH to the ecosystem for each ETH he sells.

Even market manipulators who fund FUD against ETH or short-sell, only do so to buy more ETH.

Very few whales are using DeFi right now. Plenty of room to grow.

Those whales who are using DeFi are rapidly increasing their holdings.

All things point up for ETH.