"Asia is Bidding?" The new HK law

(Translations available at:

-Korean: adamscochranKR.substack.com

-Japanese: cochranJP.substack.com

-Chinese: adamscochranZH.substack.com)

"Asia is bidding" - at least that's the current storyline here on crypto Twitter.

Partly based on excitement around Hong Kong's new laws offering clear access to crypto.

But, let's breakdown that new set of regulations that were proposed last night:

The consultation paper for VATPO (Virtual Asset Trading Platform Operators) is put out by the Securities and Futures Commission of Hong Kong, and outlines a series of proposed rules in order for anyone to offer "Virtual Assets" on a trading platform.

The first important clause is that this new set of regulations will apply to anyone:

-A) Offering services in Hong Kong

or

-B) Advertising to users in Hong Kong

Similar to the US approach of applying regulations to international companies targeting local users.

It also expressly notes, that this will apply to all types of tokens.

Traditional SFC rules only applied to tokens that were classes as "securities" under Hong Kong law, but this law will apply to everything.

In order to be licensed the SFC will require a number of components.

Custody of Assets:

The first requirement outlines how assets must be stored.

It requires exchanges to keep only 2% of assets in hot wallets and the rest to be in a cold wallet at all times.

At first this regulation seems reasonable, but it is the details that create problems.

The wording "A platform operator shall...[not]...create an encumbrance over client virtual assets" directly breaks yield programs, earn programs or exchanges offering farming services.

The details don't say "you can't do it unless the user consents" they say "you can't do it" which will block the ability for Hong Kong regulated exchanges to offer the diverse services that they have been known for.

Next this clause says "It is also required to maintain an insurance policy to cover risks associated with the custody of client virtual assets"

This also seems reasonable, except for the fact that very few existing insurance brokers are willing to cover crypto deposits.

The few that do, charge a fortune and focus on institutional clients; and they charge based on assets-under-management (AUM) not trade volume.

So the model of exchanges charging 0.05% per trade simply won't work if they are required to have insurance.

Next up, is the KYC/AML regime. At first glance it seems normal, until you realize it asks for:

-Clients financial situation

-Investment experience

-Investment objectives

-Knowledge of virtual assets

-Knowledge of risks

"before providing *ANY* service to the client*

This means HK registered exchanges will have to have the most invasive and detailed KYC/AML programs, before even allowing a client to deposit.

This is very different from the current model where they verify identities, often on withdrawals, after a certain volume.

The law also prohibits conflict of interests including trade desks and market marking activities.

This will likely include OTC offerings.

While this is a good thing for consumers, the reality is lots of exchanges drive their profits from these services.

Being unable to offer them, will likely mean a large increase in the fees associated with using HK regulated crypto exchanges.

It also broadly defines the "Platform Operator" not as the business, but as the associated entities meaning structures like FTX/Alameda, or Binance/Merit Peak, wouldn't be allowed either.

Once again, good for users, but will lead to rising costs and lower volume/liquidity in the markets as big players are forced to not market make if they want HK access.

If an exchange (crypto or traditional) follows those regulations, they'd be approved for offering limited "Virtual Asset" products, and only to sophisticated investors.

So what about "retail investors"?

SFC has allowed limited engagement of retail investors across virtual asset products.

They started in Jan 2022 with derivatives products, and October 2022 with ETF products.

During this time, only three providers were approved.

The largest of these products is the "CSOP Bitcoin Futures ETF"

Which has only $56M USD under management, despite being listed on the SEHK allowing all retail investors access to this product.

For some reason, in Western countries people believe these products are "coming soon" when the reality is they've been here for over a year, and not seen much uptick.

The SFC believes these are sufficient for retail access and so they have much stricter requirements if a crypto exchange wants to offer products to retail investors.

The first of which, is that retail users will have to pass knowledge tests or training to be allowed to use the platform:

They'll also have to validate financial circumstances, and each exchange will have to have guidelines on the maximum amount of assets a user can engage in based on their own risks

The regulations also make clear that, regulated exchanges will not be allowed to offer any token which falls under the definition of "securities" in Hong Kong

Which will preclude interest bearing, dividend distributing assets, the advertising of yields & other attributes.

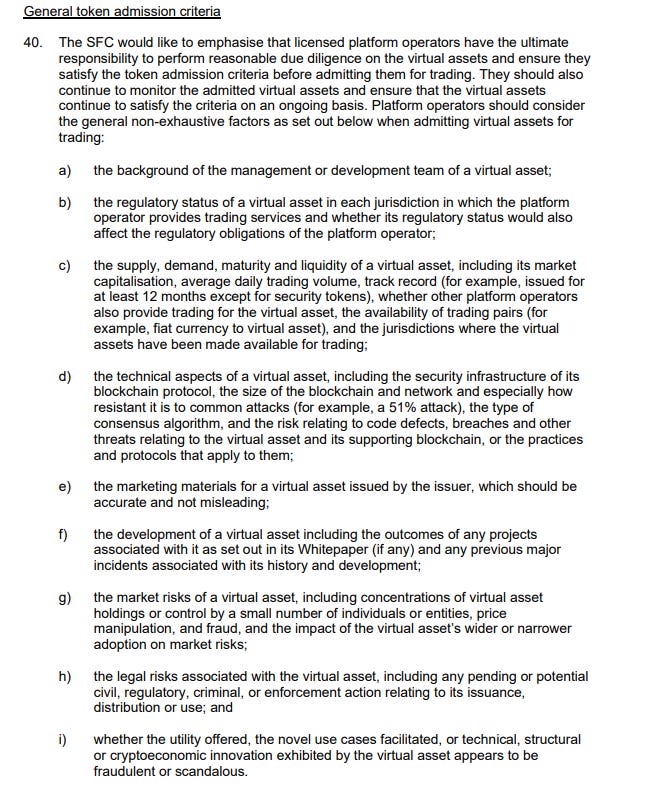

Even after all this, to list a token, the token will need to meet other requirements.

These include a 'doxxed' team with sufficient background, marketing materials that don't violate HK securities laws (no APYs), the asset is legal in the issuers jurisdiction (no US devs)

As well as an analysis of the legal risks, and if they asset is novel in its use, and not "fraudulent or scandalous" - why? Because the liability for listing such an asset will now fall to the exchange.

List something that is a scam, and you're in trouble.

This is a huge hurdle to climb, but then, the SFC notes, that these regulations are only for "sophisticated and institutional investors"

If you want to offer assets to retail investors, you require another set of guidelines.

These assets must be "Eligible large-cap virtual assets" which are included in "two acceptable indices" provided by "two independent index providers"

Currently, in HK, the only assets that meet this requirement are BTC and ETH.

Upon listing any asset, the exchange will also need to:

-Conduct their own audit of any code, or hire a third-party auditor to do that.

-Have a written memorandum from HK based legal counsel, showing a legal opinion that the asset is not a security under HK law.

Then the SFC goes on to note, that to maintain their license, no platform may offer futures or other derivatives of any kind.

Something that has been a substantial revenue driver for these exchanges.

This regulation applies to anyone targeting the HK market.

So if you want your exchange to offer trading in HK (and therefore access to China) you can't offer futures to any users, even in other countries, or else you won't meet the requirements to be a regulated entity in Hong Kong.

The SFC then proposes to rescind VATP guidelines that it previously used which exempted "asset-backed tokens" from securities regulation.

Removing this regulation, would now mean that in Hong Kong stablecoins would be seen as a security.

So any exchange wishing to have access to the Chinese market, will have to have only fiat payment systems, or have a separate securities dealer license to let "sophisticated investors" (but not retail investors) use stablecoins.

It also notes, that any tokens with voting rights, will require a platform to manage those voting rights on behalf of the user and facilitate their use.

Meaning a major technical overhaul for exchanges, figuring out how to let users vote with governance tokens.

The proposal continues on for another 300+ pages giving extensive detail on what is meant by each clause, the requirements, and the penalties.

It makes each platform liable for listing anything that is a security, any hack, or any scam they list.

It imposes weird sweeping rules on transactions, such as considering it a "conflict of interest" for an exchange to source liquidity from another platform through automation.

It ultimately makes the burdens of "Virtual Asset Operators" more extreme than running a traditional stock market exchange.

Having read through this entire document I have two conclusions:

1) HK exchanges with diverse assets, will only exist for professional investors.

2) This law is not designed to help HK/China access crypto. It's designed to be too big of a burden, so that only SEHK listed futures are accessed.

This is to ensure you feel like you get access to BTC and ETH, through futures products on a regulated exchange, but nothing more.

These requirements make it almost impossible for any exchange to operate.

And, even if an exchange can meet the regulatory requirements, they can basically only list Bitcoin and Ethereum, have to pay high cost insurance, can't accept stablecoins, and need to perform the most invasive KYC/AML on the market.

If the HK bill passes in its current form, you would be better opening up an exchange in the US, Canada or UK. While their guidelines are strict, they at least allow you to operator.

This will just drive Chinese exchanges into the ground.